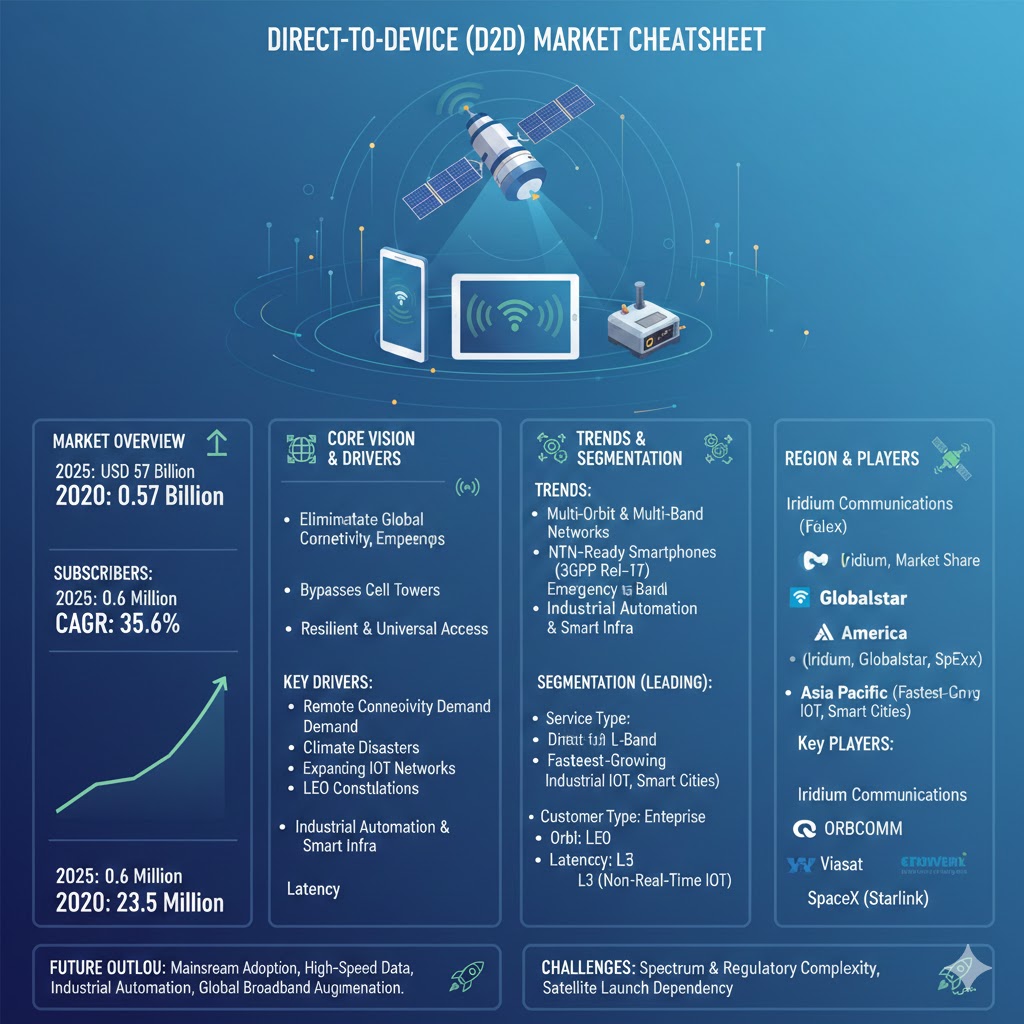

The Direct-to-Device (D2D) Market is entering a transformative phase as global connectivity evolves beyond traditional terrestrial systems and transitions toward satellite enabled communication. Estimated at USD 0.57 billion in 2025, the market is projected to reach USD 2.64 billion by 2030, expanding at an extraordinary CAGR of 35.6%. The exponential rise of D2D subscribers, especially in the consumer segment, reinforces the scale of this technological shift. Subscriber numbers are anticipated to grow from 0.6 million in 2025 to 23.5 million by 2030, marking an unprecedented adoption curve.

The core vision of the Direct-to-Device (D2D) Market is to eliminate global connectivity gaps by enabling smartphones, IoT devices, industrial equipment, and emergency response systems to communicate directly with satellites. This direct communication pathway bypasses the need for terrestrial cell towers or broadband infrastructure, making connectivity fundamentally more resilient and universally accessible. The rise of 3GPP NTN (Non Terrestrial Network) standards has enabled mass market devices to become satellite ready, propelling the Direct-to-Device (D2D) Market into mainstream telecommunications.

Growing demand for uninterrupted connectivity in remote regions, increasing climate induced disasters, expanding IoT networks, and advancements in LEO satellite constellations are driving the market forward. The Direct-to-Device (D2D) Market is no longer limited to emergency messaging or niche industrial applications. It is rapidly evolving into a global ecosystem that promises seamless, always on connectivity for billions of users worldwide.

Market Dynamics in the Direct-to-Device (D2D) Market

Growing Need for Global, Uninterrupted Connectivity

The world today relies heavily on digital networks for communication, commerce, safety, and public services. Yet more than two billion people live outside reliable terrestrial coverage zones. The Direct-to-Device (D2D) Market addresses this gap by offering satellite based connectivity directly to smartphones and IoT devices. With LEO constellations providing low latency and high coverage, D2D solutions are emerging as a key enabler of global connectivity expansion.

Acceleration in IoT and Digital Transformation

Mass adoption of IoT systems in industries such as agriculture, mining, transportation, and utilities is creating massive demand for wide area, uninterrupted coverage. IoT sensors deployed in remote environments often operate beyond the reach of terrestrial networks. The Direct-to-Device (D2D) Market solves this challenge by enabling IoT devices to communicate directly with satellites for asset monitoring, predictive maintenance, logistics automation, and environmental surveillance.

Rapid Growth in Enterprise Network Demand

Enterprises are rapidly investing in digital transformation across remote operations and mission critical environments. As a result, demand for enterprise focused D2D connectivity is surging. Businesses are adopting D2D for asset tracking, worker safety, resilient operations, and continuity during infrastructure outages. This structural shift positions enterprise networks as a major growth engine in the Direct-to-Device (D2D) Market.

Expansion of LEO Satellite Constellations

The scalability of LEO constellations is a powerful driver of future market growth. Companies such as SpaceX, AST SpaceMobile, Iridium, and Globalstar are rapidly deploying new satellites that support direct smartphone connectivity. Declining launch costs, miniaturized satellite technologies, and multi orbit network integration provide a strong foundation for the future of the Direct-to-Device (D2D) Market.

To Know About the Assumptions Considered for the Study Download the PDF Brochure

Trends Transforming the Direct-to-Device (D2D) Market

Rise of Multi Orbit and Multi Band Networks

The Direct-to-Device (D2D) Market is transitioning from single orbit to hybrid architectures integrating LEO, MEO, and GEO satellites. Multi orbit connectivity ensures broader coverage, reduced congestion, and higher reliability. Meanwhile, the increasing use of L-band, S-band, and future Ka-band systems improves resilience and capacity for both smartphone and IoT applications.

Explosion of NTN-Ready Smartphones and Devices

With growing support for 3GPP NTN Release-17 standards, smartphones from leading manufacturers are becoming capable of satellite communication without specialized hardware. This will dramatically boost adoption across consumer markets, accelerating the shift of the Direct-to-Device (D2D) Market toward mainstream connectivity.

Integration of Satellites into Emergency Connectivity Systems

Governments and telecom operators are integrating D2D into public alert systems for disaster resilience. In natural disasters, when terrestrial networks fail, satellite enabled smartphones will provide emergency SOS, location sharing, and two way messaging. This trend is becoming a defining force in the Direct-to-Device (D2D) Market.

Growth in Industrial Automation and Smart Infrastructure

Industrial sectors across remote locations are adopting D2D to automate operations, ensure worker safety, and maintain real time situational awareness. The shift toward smart agriculture, intelligent mining, and connected logistics amplifies the role of the Direct-to-Device (D2D) Market in enterprise transformation.

Restraints and Challenges

Spectrum and Regulatory Complexity

D2D operates at the intersection of terrestrial and satellite networks, creating a complex spectrum landscape. Harmonized global spectrum allocation remains one of the biggest challenges in the Direct-to-Device (D2D) Market. Coordination across regulators, satellite operators, and telecom carriers is essential to avoid interference and ensure compliance with international standards.

High Dependency on Satellite Launch Cycles

The Direct-to-Device (D2D) Market is heavily dependent on timely deployment of satellite constellations. Delays in manufacturing, launch schedules, or orbital insertion can significantly slow down commercial readiness. Operational disruptions across supply chains also pose risks for large scale deployments.

Market Segmentation of the Direct-to-Device (D2D) Market

By Service Type: Direct-to-IoT Leads the Market

The Direct-to-IoT segment is anticipated to account for the largest share of the Direct-to-Device (D2D) Market. Demand from industries requiring remote asset connectivity, continuous monitoring, and large scale sensor deployments is fueling strong adoption.

By Frequency: L-Band Dominance

L-band frequencies are projected to hold the largest market share due to their resilience in adverse weather conditions, minimal signal attenuation, and proven suitability for mobile and IoT communication systems. This reliability positions L-band as the core frequency for mainstream D2D services.

By Customer Type: Enterprise Networks Leading

Enterprise customers represent the biggest share of the Direct-to-Device (D2D) Market. Enterprises depend on wide area, continuous connectivity for predictive maintenance, fleet management, remote operations, and automated industrial workflows.

By Orbit: LEO Segment Dominates

Low Earth Orbit satellites offer low latency and improved network performance. Their growing deployment enables real time communication for smartphones and IoT devices, making LEO the dominant orbit type in the Direct-to-Device (D2D) Market.

By Latency Class: L3 Segment Strongest

The L3 latency class is preferred for IoT and non real time applications requiring intermittent data transfer. Its lower infrastructure demand and cost efficiency make it ideal for broad industrial adoption.

Regional Outlook of the Direct-to-Device (D2D) Market

North America: Largest Market Share

North America is expected to hold the largest share of the Direct-to-Device (D2D) Market due to a strong ecosystem of satellite operators, telecommunications innovators, and regulatory support. Companies such as Iridium, Globalstar, and SpaceX contribute significantly to regional leadership.

Asia Pacific: Second Fastest Growing Region

Asia Pacific’s expanding mobile subscriber base, industrial digitalization, and emerging smart city networks make it the second fastest growing region. Demand for agricultural IoT, logistics automation, and emergency connectivity fuels the region’s rapid adoption.

Key Players in the Direct-to-Device (D2D) Market

Iridium Communications Inc.

Iridium is a global leader in L-band satellite communication. Its resilient architecture, global coverage, and advanced satellite technologies make it the strongest player in the Direct-to-Device (D2D) Market. Iridium is deeply involved in emergency connectivity, IoT communications, and enterprise applications.

Globalstar

Globalstar provides satellite-to-device services supporting emergency messaging, IoT tracking, and enterprise connectivity. Its L/S-band infrastructure and increasing partnerships with telecom operators position it as a major contributor to the D2D ecosystem.

ORBCOMM

ORBCOMM offers satellite enabled IoT solutions across logistics, fleet monitoring, maritime operations, and industrial automation. Its efficient, high capacity connectivity platforms strengthen its role in the Direct-to-Device (D2D) Market.

Viasat

Viasat provides advanced satellite connectivity services supporting enterprise networks, consumer applications, and aviation. Its expansion into hybrid satellite cellular architectures aligns strongly with the future trajectory of the Direct-to-Device (D2D) Market.

SpaceX

SpaceX’s Starlink constellation is rapidly developing capabilities to enable satellite-to-cellular communication for both IoT and mainstream smartphones. Its scale, innovation speed, and multi orbit architecture position it as a rising leader in the D2D landscape.

Future Outlook of the Direct-to-Device (D2D) Market

The Direct-to-Device (D2D) Market is on the verge of mainstream adoption as satellite enabled devices become standard features in consumer smartphones, industrial sensors, and enterprise systems. Large scale deployment of LEO constellations, multi orbit integration, enhanced spectrum harmonization, and advances in NTN standards will open new opportunities across industries, governments, disaster management agencies, and the global connectivity ecosystem.

D2D services will evolve beyond emergency messaging into high speed data services, industrial automation, remote workforce support, and global broadband augmentation. As the world moves toward universal connectivity, the Direct-to-Device (D2D) Market will become one of the most transformative segments within the broader satellite communication industry.

Related Report:

Direct-to-Device (D2D) Market by Service Type (Direct to IoT, Direct to Cell), Customer Type (Consumer, Enterprise Network, Government & Defense), Latency Class, Frequency, Orbit and Region – Global Forecast to 2030