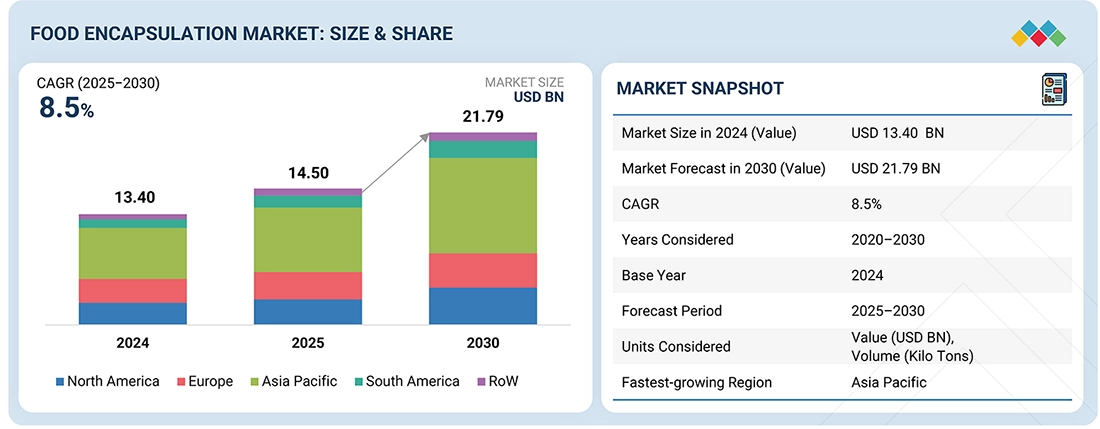

The global food encapsulation market was valued at USD 14.50 billion in 2025 and is projected to reach USD 21.79 billion by 2030, growing at a CAGR of 8.5% from 2025 to 2030. Food encapsulation is a rapidly growing market, with the food and nutrition industry increasingly adopting this technology to ensure the stability of ingredients, enhance shelf life, and enhance functional performances. Encapsulation helps to save active ingredients that are sensitive to heat, moisture, oxygen, and other process stress, ensuring delivery as well as consistency throughout the lifecycle of a product. This gives significant support for functional foods, fortified foods, dietary supplements, infant nutrition, and pet food, where monotony and nutritional efficacy are of utmost centrality. Additionally, the market thrives due to the increased consumer hunger for clean-label, health-oriented, and preventive food products. Mostly, flavor matching, controlled release, and highly consistent distribution make encapsulation desirable for manufacturers to fulfill regulatory requirements with the undiminished feasibility of their products. Through technologies such as spray-drying, fluid-bed coating, coacervation, and lipid-based encapsulation that are constantly improving by providing scalability and cost effectiveness.

Established companies like Nestlé, Danone, Kerry Group, DSM-Firmenich, Ingredion, BASF, and Cargill have played significant roles in offering application-specific encapsulated ingredients and channeling efforts towards process optimization, formulation stability, and regional capacity expansion. With North America and Europe being long-time established markets due to mature functional food industries, the Asia Pacific is emerging as a high-growth region driven by rising health awareness, urbanization, and increased consumption of fortified and functional foods.

Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=68

By shell material, the polysaccharides segment accounts for the largest market share.

Polysaccharides are the major shell material in the food encapsulation market, with a large market share due to broad regulatory approval, multiple functionalities, and application possibilities in different food matrices. There are quite a number of polysaccharides used as vitamins, minerals, flavors, probiotics, and bioactive compounds, including maltodextrin, modified starch, arabic gum, alginate, pectin, and cellulose derivatives. Their ability to form films and solubilize and also protect the thermally unstable compounds from heat, oxygen, and moisture provides them with opportunities in large-scale applications for various food developments. Moreover, they support clean labeling and plant-based positioning, which is important for the fortified and functional foods market. Polysaccharides may be used to achieve a controlled release of actives, maintain complete dispersion, and provide sensory neutrality in bakery products, dairy replacements, drinks, and hyper-proposed items. Polysaccharide shells are very conducive to these markets, as they are cost-effective, highly scalable, and well-matched with omnipresent methodologies of shell creation, namely spray drying and fluid-bed coating.

By technology, the microencapsulation segment accounts for the largest market share.

In the food encapsulation market, the use of microencapsulation is attributed to its widespread application, technical reliability, and compatibility with the large-scale food processing process. Techniques such as spray drying, fluidized powders, coacervation, and extrusion can be integrated into the existing food processing lines, allowing manufacturers to encapsulate sensitive ingredients at a commercial scale with consistent quality and cost control. These techniques are widely used in the protection of vitamins, minerals, flavors, probiotics, omega-3, and organic acids from heat, moisture, oxygen, and mechanical degradation.

Microencapsulation, a technique employed by the food industry, enables the controlled release of active ingredients at the desired places and times, increases a product’s shelf life, and thus improves its handling and stability, vital applications in functional foods, dietary supplements, bakery and dairy products, infant nutrition, and clinical nutrition. This technology also supports taste masking and odor control, a strong support for excellent sensory quality while maintaining the nutritional standard for any of the products developed by the industry. Unlike nanoencapsulation, microencapsulation avails a clearer path for regulatory acceptance of encapsulants that have a demonstrated safety record and reasonable production complexity; thus, it is the obvious choice for food-grade applications.

Request Sample Pages: https://www.marketsandmarkets.com/requestsampleNew.asp?id=68

Based on region, North America accounts for the largest market share.

North America holds the largest share, mainly because the functional food ecosystem is truly advanced in this region, besides intense consumer awareness of foods for nutraceuticals and the lofty presence of huge companies providing food and ingredients. The US, as a major country of food-encapsulated products with almost all varieties, boasts strong professional standards in fortified foods, dietary supplements, clinical nutraceuticals, and special food products, where encapsulation is widely used to improve stability, controlled release, and shelf life of the functional elements. High intake of vitamins, minerals, omega-3, probiotics, and bioactive compounds, having crossed the practical threshold into an almost everyday food format, reinforces the adaptation to food encapsulation technology in all product categories.

Apart from the advanced food processing infrastructure, the region had an early experience with the operation at a commercial scale of encapsulation technology, which has been useful for different kinds of food products. A well-established regulatory framework, including food ingredient and fortification issues, makes the system quite open. They intend to make the system as innovative as possible while maintaining all the safety and quality standards. Considering the same, the leading global financial players on the front lines of this field, DSM-Firmenich, Ingredion, Cargill, ADM, and Kerry, maintain significant R&D and manufacturing facilities and application development capability in North America, thereby further solidifying the region’s position as a global leader. Therefore, the continuous innovation on value-added products and clean-label reformulation, and the rising demand for convenience nutrition solutions are considered to dominate and uphold the position of North America in the food encapsulation market over the near future.

Leading Food Encapsulation Companies:

The report profiles key players such as DSM-Firmenich (Switzerland), Givaudan (Switzerland), International Flavors & Fragrances (IFF) (US), Kerry Group (Ireland), Archer Daniels Midland (ADM) (US), BASF SE (Germany), Cargill, Incorporated (US), Ingredion Incorporated (US), Tate & Lyle PLC (UK), and Sensient Technologies Corporation (US).