The Rise of Smart EW and Counter-UAV Systems in Autonomous Warfare Operations

Smart Electronic Warfare (EW) and Counter UAV Systems Market Summary

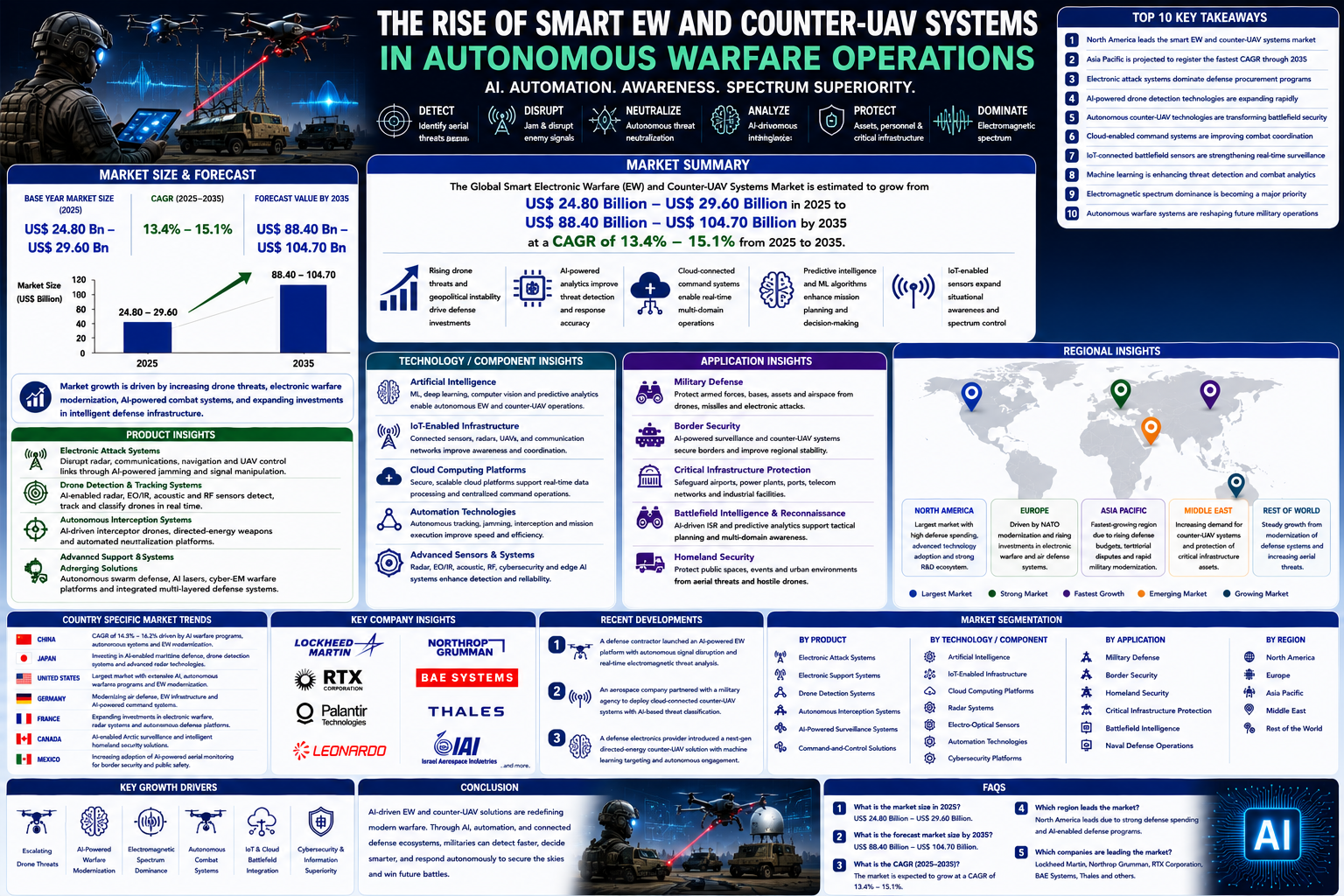

The Global Smart Electronic Warfare (EW) and Counter UAV Systems Market is estimated to grow from US$ 24.80 Billion – US$ 29.60 Billion in 2025 to US$ 88.40 Billion – US$ 104.70 Billion by 2035 at a CAGR of 13.4% – 15.1% from 2025 to 2035. The rapid expansion of autonomous warfare operations, increasing drone-based threats, and rising geopolitical tensions are significantly accelerating demand for intelligent defense systems worldwide. Governments and military organizations are increasingly investing in AI-powered electronic warfare platforms, autonomous drone interception systems, electromagnetic spectrum dominance technologies, and cloud-connected command infrastructures to enhance battlefield superiority and operational efficiency. The integration of artificial intelligence, IoT-enabled battlefield surveillance, machine learning-based threat analytics, and automated combat systems is reshaping modern military doctrine and creating a new generation of smart defense ecosystems capable of real-time decision-making and autonomous response capabilities.

Key Market Trends & Insights

North America remains the dominant regional market due to strong investments in AI-enabled military modernization and autonomous warfare technologies.

Asia Pacific is projected to register the fastest growth driven by rising defense expenditures and increasing regional security challenges.

Electronic attack and autonomous drone detection systems continue to dominate global procurement programs.

AI-powered battlefield analytics and machine learning-enabled threat recognition systems are emerging as major technology trends.

Cloud-based military command-and-control platforms are improving real-time operational coordination and multi-domain warfare capabilities.

Automation and IoT-enabled surveillance infrastructure are accelerating the development of autonomous defense ecosystems worldwide.

Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=4197284

Market Size & Forecast

- Base year market size (2025): US$ 24.80 Billion – US$ 29.60 Billion

- Forecast value by 2035: US$ 88.40 Billion – US$ 104.70 Billion

- CAGR (2025–2035): 13.4% – 15.1%

- Market growth is supported by increasing drone warfare threats, AI-driven defense modernization programs, rising demand for autonomous combat systems, and advancements in intelligent electronic warfare technologies

AI-Powered Military Transformation: The Future of Smart Combat and Defense Top 10 Key Takeaway

- North America leads the smart EW and counter-UAV systems market

- Asia Pacific is expected to witness the highest CAGR through 2035

- Electronic attack systems dominate defense modernization programs

- AI-powered drone detection technologies are expanding rapidly

- Autonomous warfare systems are transforming military operations

- Cloud-enabled command systems are improving combat coordination

- IoT-connected battlefield sensors are strengthening defense intelligence

- Machine learning is enhancing threat detection and combat analytics

- Counter-drone technologies are becoming essential for national security

- Intelligent EW systems are reshaping future battlefield strategies

Product Insights

Electronic attack systems represent the largest product segment within the smart EW and counter-UAV systems market. Defense organizations globally are prioritizing advanced electronic attack capabilities to disrupt enemy communication systems, navigation infrastructure, radar networks, and autonomous aerial operations. AI-powered signal jamming technologies, adaptive electromagnetic disruption platforms, and autonomous spectrum management systems are becoming critical components of modern military operations.

Counter-UAV detection systems are also witnessing substantial demand as unmanned aerial threats become increasingly sophisticated and accessible. Military agencies are deploying AI-enabled radar systems, electro-optical sensors, infrared tracking technologies, and acoustic detection solutions capable of identifying, tracking, and classifying drones in real time. The integration of machine learning algorithms significantly improves target identification accuracy and response efficiency under dynamic battlefield conditions.

Autonomous interception systems are emerging as one of the fastest-growing product categories in the market. Intelligent interceptor drones, directed-energy weapons, automated missile defense systems, and AI-enabled kinetic neutralization technologies are supporting rapid-response battlefield operations while minimizing human involvement in high-risk combat environments.

Electronic support systems are increasingly being adopted for signal intelligence, battlefield reconnaissance, and electromagnetic spectrum monitoring applications. AI-powered analytics platforms help military operators identify hostile communication patterns, assess threat environments, and improve tactical situational awareness across multi-domain combat operations.

Future product development is expected to focus on AI-powered drone swarm defense systems, autonomous electromagnetic warfare infrastructure, next-generation directed-energy weapons, and integrated battlefield intelligence ecosystems capable of supporting highly automated warfare operations.

Technology / Component Insights

Artificial intelligence is serving as the foundation of next-generation electronic warfare and counter-UAV technologies. AI-powered algorithms support autonomous target recognition, predictive threat analytics, adaptive signal jamming, and real-time battlefield decision-making. Machine learning and deep learning technologies enable defense systems to continuously improve operational performance by analyzing combat data and evolving threat patterns.

IoT-enabled defense infrastructure is significantly improving military connectivity and operational synchronization across complex battlefield environments. Connected sensors, surveillance systems, autonomous drones, radar networks, and command platforms allow seamless real-time communication between defense assets while improving situational awareness and mission coordination.

Cloud computing technologies are increasingly supporting military command-and-control operations by enabling centralized battlefield data management and secure intelligence sharing. Cloud-based defense ecosystems improve scalability, operational flexibility, and rapid deployment capabilities for autonomous combat operations.

Automation technologies are revolutionizing modern warfare through autonomous surveillance systems, automated drone interception platforms, AI-powered electronic attack operations, and intelligent mission execution systems. Automated combat infrastructure improves operational speed, reduces human workload, and enhances defense responsiveness during high-intensity conflict scenarios.

Advanced radar systems, cybersecurity platforms, electro-optical imaging technologies, edge AI processors, and secure communication infrastructure are also critical components of intelligent warfare ecosystems. AI-powered sensor fusion technologies combine multiple battlefield inputs into unified operational intelligence systems that support faster and more accurate military decision-making.

Future innovation trends are expected to include quantum-enabled defense computing, autonomous drone swarm management systems, AI-driven cyber-electromagnetic warfare platforms, and next-generation intelligent combat ecosystems designed for multi-domain autonomous warfare operations.

Application Insights

Military defense applications account for the largest share of the smart EW and counter-UAV systems market due to rising investments in autonomous warfare modernization and intelligent battlefield security infrastructure. Armed forces worldwide are rapidly deploying AI-powered surveillance systems, electronic warfare technologies, autonomous combat platforms, and integrated command-and-control systems to strengthen operational effectiveness and strategic defense readiness.

Border security and homeland defense applications are emerging as major growth areas due to increasing drone-related security concerns and rising cross-border surveillance requirements. Governments are investing heavily in AI-enabled drone detection platforms, automated monitoring systems, and intelligent perimeter security infrastructure to protect military facilities, airports, critical infrastructure, and urban environments.

Battlefield intelligence and reconnaissance operations are also experiencing strong market demand due to the growing need for real-time combat awareness and predictive threat analysis. AI-powered battlefield analytics platforms enable faster tactical decision-making while improving multi-domain operational coordination across air, land, sea, cyber, and space environments.

Critical infrastructure protection is becoming an increasingly important application segment as governments and commercial operators seek advanced solutions to secure energy facilities, communication networks, transportation hubs, and industrial assets from drone-based threats and electronic warfare disruptions.

Future opportunities are expected to emerge across naval defense systems, smart city security infrastructure, autonomous air defense networks, and AI-powered cyber-electromagnetic warfare operations.

Regional Insights

North America dominates the global smart EW and counter-UAV systems market due to strong military spending, rapid adoption of AI-powered defense technologies, and extensive investments in autonomous warfare infrastructure. The United States continues to lead innovation in intelligent battlefield systems, electronic attack technologies, and autonomous drone defense platforms. The region’s strong defense industrial base and ongoing modernization programs are supporting long-term market expansion.

Europe remains a strategically important market driven by increasing defense collaboration, NATO modernization initiatives, and growing investments in AI-enabled battlefield security systems. Countries including Germany, France, and the United Kingdom are focusing on electronic warfare modernization, autonomous surveillance technologies, and integrated air defense infrastructure to strengthen regional security preparedness.

Asia Pacific is expected to witness the fastest market growth through 2035 due to rising geopolitical tensions, expanding military budgets, and increasing investments in autonomous combat systems. China, Japan, India, and South Korea are rapidly deploying AI-driven warfare technologies, smart drone defense infrastructure, and advanced electronic warfare systems to strengthen national defense capabilities.

The Middle East is also witnessing rising demand for intelligent EW and counter-UAV systems due to growing investments in border security, critical infrastructure protection, and autonomous aerial surveillance operations.

- North America remains the global leader in intelligent warfare modernization

- Asia Pacific is projected to achieve the highest growth through 2035

- Europe is accelerating investments in autonomous battlefield technologies

- AI-powered drone defense systems are expanding rapidly worldwide

- Cloud-connected combat infrastructure is transforming defense operations

Country Specific Market Trends

China is projected to grow at a CAGR of 14.5% – 16.2% from 2025 to 2035 due to increasing investments in AI-enabled defense ecosystems, autonomous drone technologies, and intelligent electronic warfare systems. The country continues to prioritize military AI integration and electromagnetic warfare modernization.

Japan is strengthening deployment of AI-powered maritime defense systems, autonomous surveillance technologies, and advanced drone interception infrastructure to improve regional security preparedness and combat readiness.

The United States remains the largest individual market globally due to strong defense spending, extensive AI research programs, and rapid deployment of autonomous warfare technologies. Canada is investing in intelligent Arctic surveillance systems and next-generation homeland security infrastructure, while Mexico is expanding AI-enabled border monitoring and aerial security capabilities.

Germany and France are increasing investments in electronic warfare modernization, intelligent battlefield coordination systems, and AI-powered defense technologies to strengthen European military readiness and NATO interoperability.

- China is rapidly expanding autonomous warfare capabilities

- Japan is modernizing intelligent maritime defense infrastructure

- The United States leads global innovation in AI-enabled combat systems

- Germany and France are strengthening electronic warfare modernization

- Canada is investing in intelligent surveillance and homeland security systems

Key Company Insights

Major companies operating in the smart EW and counter-UAV systems market include Lockheed Martin, Northrop Grumman, RTX Corporation, BAE Systems, Leonardo, Thales, Israel Aerospace Industries, and Rheinmetall.

These companies are focusing heavily on AI-powered electronic warfare systems, autonomous drone interception technologies, cloud-based battlefield command infrastructure, and integrated electromagnetic warfare solutions. Strategic defense partnerships, military contracts, and research collaborations are helping accelerate innovation across intelligent combat systems and autonomous defense ecosystems.

Manufacturers are increasingly prioritizing AI-driven surveillance technologies, automated signal intelligence platforms, cyber-electromagnetic warfare systems, and multi-domain autonomous operations to strengthen competitive positioning and long-term market growth.

- AI-enabled battlefield analytics remain a major innovation priority

- Autonomous counter-UAV technologies are attracting strong investments

- Electronic warfare modernization is accelerating global competition

- Cloud-connected defense ecosystems are improving operational efficiency

- Strategic partnerships are supporting rapid defense technology deployment

Recent Developments

A leading defense technology provider recently launched an AI-powered counter-UAV platform capable of autonomous drone detection, threat classification, and real-time interception in contested combat environments.

A major aerospace company partnered with a military agency to develop cloud-connected electronic warfare infrastructure integrated with AI-enabled battlefield analytics and autonomous spectrum management capabilities.

An advanced defense electronics manufacturer introduced a next-generation directed-energy counter-drone system featuring machine learning-powered targeting and automated electromagnetic disruption technologies.

Market Segmentation

The smart EW and counter-UAV systems market is segmented by product, technology/component, application, and region. By product, the market includes electronic attack systems, electronic support platforms, autonomous interception systems, AI-powered drone detection technologies, command-and-control systems, and intelligent surveillance infrastructure. Electronic attack systems continue to dominate due to increasing military investments in electromagnetic spectrum superiority.

By technology/component, the market includes artificial intelligence, IoT-enabled communication systems, cloud computing platforms, automation technologies, advanced radar systems, electro-optical sensors, and cybersecurity infrastructure. AI-powered analytics and autonomous combat systems are expected to witness the highest growth over the forecast period.

By application, the market covers military defense, homeland security, battlefield intelligence, border surveillance, critical infrastructure protection, and naval defense operations. Military defense remains the dominant application segment due to rapid deployment of intelligent combat systems and autonomous battlefield operations.

Regionally, the market is segmented into North America, Europe, Asia Pacific, and the rest of the world. North America currently leads global revenues, while Asia Pacific is projected to emerge as the fastest-growing market through 2035.

- Electronic attack systems dominate global procurement programs

- AI-powered drone detection technologies are expanding rapidly

- Military defense remains the largest application segment globally

- Autonomous combat systems are reshaping battlefield operations

- Asia Pacific is expected to witness the fastest regional growth

Conclusion

The rise of smart electronic warfare and counter-UAV systems is fundamentally reshaping the future of autonomous warfare operations and intelligent battlefield security. Rapid advancements in artificial intelligence, IoT-enabled defense infrastructure, automation technologies, and cloud-connected military ecosystems are accelerating the evolution of next-generation combat operations.

As global defense organizations continue prioritizing autonomous warfare modernization and electromagnetic spectrum dominance, demand for intelligent EW and counter-drone technologies is expected to grow significantly through 2035. Companies capable of delivering AI-powered battlefield analytics, autonomous interception systems, intelligent surveillance infrastructure, and integrated combat ecosystems will remain strategically positioned to lead the next era of global defense innovation.

FAQs

1. What is the market size of the smart EW and counter-UAV systems market?

The market is estimated to grow from US$ 24.80 Billion – US$ 29.60 Billion in 2025 to US$ 88.40 Billion – US$ 104.70 Billion by 2035.

2. What is the expected growth rate of the market?

The market is projected to grow at a CAGR of 13.4% – 15.1% from 2025 to 2035.

3. What are the key drivers of the market?

Key drivers include increasing drone warfare threats, rising investments in autonomous combat systems, AI-powered defense modernization, and expanding electronic warfare capabilities.

4. Which region leads the global market?

North America currently leads the market due to strong military spending and rapid deployment of AI-enabled defense technologies.

5. Which companies are leading the market?

Leading companies include Lockheed Martin, Northrop Grumman, RTX Corporation, BAE Systems, and Thales.