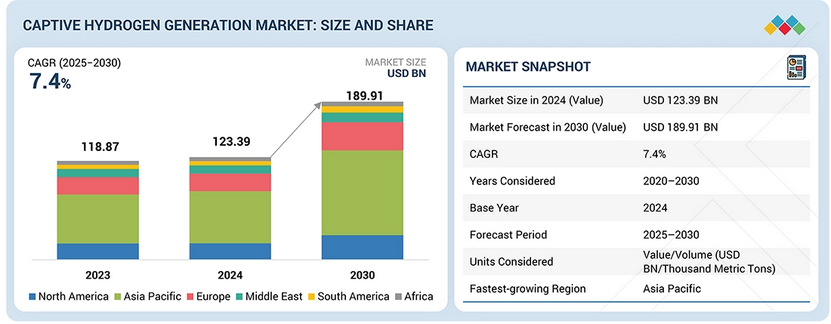

The report “Captive Hydrogen Generation Market by Source (Blue, Green, Gray), Application (Refinery, Ammonia, Methanol, Transportation, Power Generation), Region – Global Forecast to 2030″ is projected to reach USD 189.91 billion by 2030 from USD 123.39 billion in 2024, at a CAGR of 7.4%.

The generation of captive hydrogen is growing at an accelerating rate due to the high industrial demand for hydrogen as well as the need for a stable on-site supply chain of hydrogen for industries such as refining, chemicals, steel, and ammonia. Many companies are investing in dedicated hydrogen systems to decrease their reliance on outside suppliers of hydrogen, improve cost stability, and provide for continuous operation. The increased focus on decarbonization has created an opportunity to develop low-carbon technologies like electrolysis and carbon capture within captive hydrogen systems, thus creating a more sustainable energy supply chain. Industrial facilities continue to produce large quantities of hydrogen at their facilities, primarily for use in refining and chemical production, which provides an opportunity to transition from traditional hydrogen to cleaner, alternative sources of hydrogen. Additionally, the increased demand for hydrogen from new applications such as transportation and distributed energy systems is creating an additional incentive to expand opportunities for captive hydrogen generation.

Download PDF Brochure @ https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=249869238

The blue hydrogen segment is projected to record the second-highest CAGR in the captive hydrogen generation market, by Source, during the forecast period.

Blue hydrogen is forecast to demonstrate the second-highest CAGR in the captive hydrogen generation market as the emphasis on carbon emission reduction of current grey hydrogen production systems increases. The incorporation of carbon capture, utilization, and storage technology with on-site hydrogen production will assist the industry in transitioning to lower-carbon operations. In addition to these developments, the heightened enforcement of environmental regulations and commitment from companies to reduce their carbon footprint are leading to further use of blue hydrogen in captive facilities. In conjunction with these developments, significant investment in CCUS infrastructure and retrofitting of existing hydrogen facilities are supporting the expansion of this segment.

The ammonia production segment, by application, is expected to hold the second-largest share of the captive hydrogen generation market throughout the forecast period.

Ammonia has the second-largest share of the market, primarily due to the continued market demand for hydrogen as a critical feedstock for the incorporation of ammonia through synthesis processes. Large-scale fertilizer manufacturing operations utilize on-site hydrogen generation as an important resource to remain competitive while also effectively conducting their operations. Furthermore, many of the integrated chemical complexes provide additional support to the usage of captive hydrogen for ammonia production applications. As agricultural productivity and the establishment of food security continue to be a focus, hydrogen will support ammonia production efforts into the foreseeable future through consistent and reliable demand. The ongoing advancement of ammonia production technologies, along with the growth of low-carbon hydrogen, will support the expansion of the ammonia segment.

Ask For Sample Pages of the Report @ https://www.marketsandmarkets.com/requestsampleNew.asp?id=249869238

Key Market Players

Many companies are involved in generating hydrogen around the world, including Chevron Corporation (US), and Exxon Mobil Corporation (US), Shell plc (UK), BP p.l.c. (UK), and ENGIE (France), Iwatani Corporation (Japan), TotalEnergies (France), Saudi Arabian Oil Co. (Saudi Arabia), and Reliance Industries Limited (India), among others.