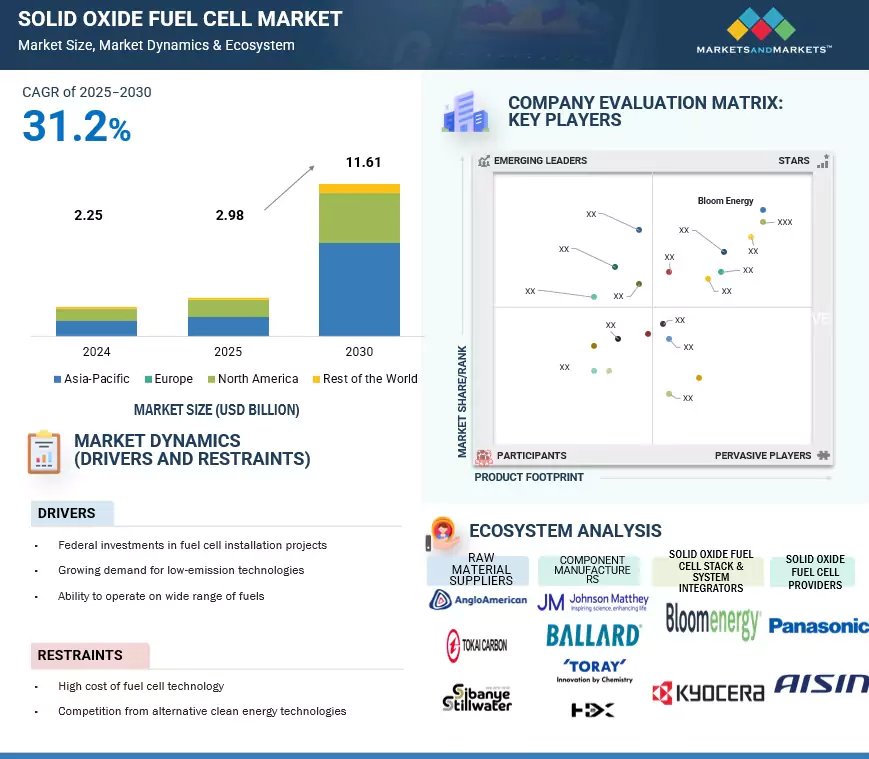

The global solid oxide fuel cell market is projected to reach USD 11.61 billion by 2030 from USD 2.98 billion in 2025, registering a CAGR of 31.2%.

The Solid Oxide Fuel Cell (SOFC) market is being shaped by rising global interest in clean, efficient, and decentralized energy solutions, driven by the dual pressures of carbon neutrality commitments and energy security concerns. Unlike conventional power systems, SOFCs offer high electrical efficiency, fuel flexibility, and low emissions, making them well-suited for a variety of applications—from residential and commercial power to industrial backup systems and emerging hydrogen infrastructures. As governments and private sector players accelerate the energy transition, supportive policies, research funding, and net-zero strategies are boosting investments in fuel cell technology. Countries in Asia Pacific, North America, and Europe are in charge of pilot projects, commercialization programs, and public–private partnerships focused on deploying SOFC systems at scale.

Download PDF Brochure – https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=39365796

By type

Development of planar SOFCs is driven by their structural advantages and applicability in various stationary and distributed power applications. A planar SOFC is constructed from a flat stack of electrolytes and electrodes, allowing for good heat and mass transfer and increased power density and efficiency rates. Planar SOFCs are easily developed into compact and modular formats, making them viable options for commercial buildings, industrial sites, and combined heat and power (CHP) applications. Residential applications are somewhere in between low-cost, scalable deployments that are common in large-scale utility configurations. Another key growth driver for the planar segment is other recent advancements in ceramic materials, the overall stack design, and sealing materials, allowing for opposite travel, increased durability, and thermal cycling. As also mentioned, the manufacturers of planar SOFCs are focused on designing more cost-effective planar designs while having fuel flexibility with hydrogen and natural gas. The tubular segment in the Solid Oxide Fuel Cell (SOFC) market is gaining traction due to its robust mechanical strength, high thermal stability, and ease of sealing compared to planar configurations. Tubular SOFCs offer excellent resistance to thermal cycling and are less prone to gas leakage, making them suitable for continuous, high-temperature operations. Although they typically have lower power densities than planar designs, their reliability and durability make them ideal for long-term industrial and off-grid applications.

By end user

The growth is largely due to the ongoing demand for reliable, efficient, and cleaner power sources to accommodate the growing digital infrastructure. With companies building more data centers to handle increasing internet traffic, cloud computing, and all workloads related to artificial intelligence, a clear push is evident to decrease emissions and increase energy security. SOFCs are a reliable supply of power with lower emissions, which is especially important for data centers that operate 24/7, as any failure from the system means a potential catastrophe. SOFCs use natural gas, biogas, or hydrogen with flexibility while helping organizations reach their sustainability targets. Furthermore, their comparatively small footprint and lower noise profile might make them suitable for urban areas or developing projects in remote locations. As more companies implement green and resilient energy strategies, the SOFC option is becoming an increasingly viable choice for data centers and other operators needing to minimize risk while positioning themselves for the energy future. This is expected to drive spirited growth in the segment over time.

Make an Inquiry – https://www.marketsandmarkets.com/Enquiry_Before_BuyingNew.asp?id=39365796

Regional Analysis

Countries such as Japan and South Korea are leading the way for SOFC deployment, particularly in residential and commercial combined heat and power (CHP) systems. In Japan, the ENE-FARM program and a supportive national framework for fuel cell uptake in homes have led to widespread SOFC uptake. Additionally, there is a strong supply chain of key players in Asia Pacific that enables the scale-up of manufacturing and deployment of SOFC technology. Hydrogen has strong support as a future fuel source in Asia Pacific, making SOFCs even more appealing as they can run efficiently on hydrogen, natural gas, and biogas. Utility prices are rising, grid stability is becoming an issue, and carbon reduction commitments are being addressed with some investment into SOFCs in residential energy, commercial backup power, and industrial use. Because of the existing policies in place, local capabilities that have been developed, and growing demand for cleaner energy technologies, the Asia Pacific region is leading SOFC development and is likely to continue doing so for the next few years.

Key Market Players

The solid oxide fuel cell market is dominated by major players with a wide regional presence. Some key players in the market are Bloom Energy (US), Mitsubishi Heavy Industries, Ltd. (Japan), AISIN Corporation (Japan), and Kyocera Corporation (Japan).