The global stem cell banking market is projected to reach USD 9.30 Billion by 2023 from 6.28 Billion in 2018, at a CAGR of 8.2%.

Factors such as the growing public awareness about the therapeutic potential of stem cells; development of novel technologies for stem cell preservation, processing & storage; rising number of hematopoietic stem cell transplantations (HSCTs); and increasing investments in stem cell-based research are driving the growth of the market. However, the high operational costs associated with stem cell banking and stringent regulatory frameworks are expected to limit the growth of the stem cell banking market during the forecast period.

Factors such as the growing public awareness about the therapeutic potential of stem cells; development of novel technologies for stem cell preservation, processing & storage; rising number of hematopoietic stem cell transplantations (HSCTs); and increasing investments in stem cell-based research are driving the growth of the market. However, the high operational costs associated with stem cell banking and stringent regulatory frameworks are expected to limit the growth of the stem cell banking market during the forecast period.

Download the PDF Brochure for More Details@ http://bit.ly/2xiA0Yg

Analysis of the market developments between 2015 and 2018 reveals that several growth strategies such as service launches & upgrades; agreements, partnerships, & collaborations; and mergers & acquisitions were adopted by the market players to strengthen and competitive position in the global stem cell banking market. Among these business strategies, agreements, partnerships, & collaborations were the most widely adopted growth strategies by majority of market players worldwide.

The global stem cell banking market is projected to reach USD 9.30 Billion by 2023 from USD 5.84 Billion in 2017; growing at a CAGR of 8.2%.

Base Year: 2017

Forecast Period: 2018–2023

Objectives of the study are:

- To define, describe, and forecast the stem cell banking market by source, service type, application, and region

- To provide detailed information about factors influencing market growth (drivers, restraints, opportunities, and industry-specific challenges)

- To strategically analyze micromarkets with respect to individual growth trends, prospects, and contributions to the overall stem cell banking market

- To analyze the market opportunities for stakeholders and provide details of the competitive landscape for key players

- To forecast the market size for North America, Europe, Asia Pacific, and the Rest of the World (RoW)

- To profile key players and comprehensively analyze their global market shares and core competencies

- To track and analyze strategic developments such as service launches & upgrades; agreements, partnerships, & collaborations; and mergers & acquisitions in the global market

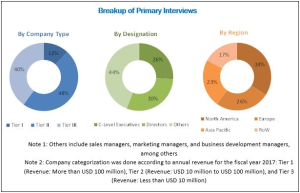

This research study involves the extensive usage of secondary sources, directories, and databases (such as, Bloomberg Business, Factiva, and Dun & Bradstreet), in order to identify and collect information useful for this technical, market-oriented, and financial study of the stem cell banking market. In-depth interviews were conducted with various primary respondents, including subject-matter experts (SMEs), C-level executives of key market players, and industry consultants to obtain and verify qualitative and quantitative information and to assess market prospects.

Read the Detailed Research report@ http://bit.ly/2PHGTsT

In 2017, Cord Blood Registry (CBR) Systems (US), Cordlife Group Limited (Singapore), and Cryo-Cell International (US) held the leading position in the global stem cell banking market. In the past three years, these companies have adopted service launches & upgrades; agreements, partnerships, & collaborations; and mergers & acquisitions as their key business strategies to ensure their market dominance. Moreover, ViaCord (US), Cryo-Save AG (Netherlands), LifeCell International (India), StemCyte (US), Global Cord Blood Corporation (China), Smart Cells International (UK), Vita34 AG (Germany), and CryoHoldco (Mexico) were some of the other major players in this market, as of 2017.

Major Market Stakeholders

- Private, public, and community stem cell banks, tissue banks, and biobanks

- Stem cell associations and organizations

- Government regulatory authorities

- Regenerative medicine and cellular therapy manufacturers

- Pharmaceutical & biopharmaceutical product manufacturers

- Healthcare service providers (including hospitals, surgical centers, and dental clinics)

- National and regional research boards and organizations

- Research and development (R&D) companies

- Clinical research organizations (CROs)

- Research laboratories and academic institutes

- Government payers and private insurance companies

- Market research and consulting firms