The Drone Detection Market is witnessing unprecedented growth, fueled by the rapid expansion of drone usage across both commercial and defense sectors. With drones becoming increasingly accessible, their misuse has created pressing security challenges. From unauthorized surveillance and smuggling to disruptions in restricted airspace, the risks associated with unregulated drone activities have compelled governments, businesses, and defense agencies to adopt advanced detection technologies.

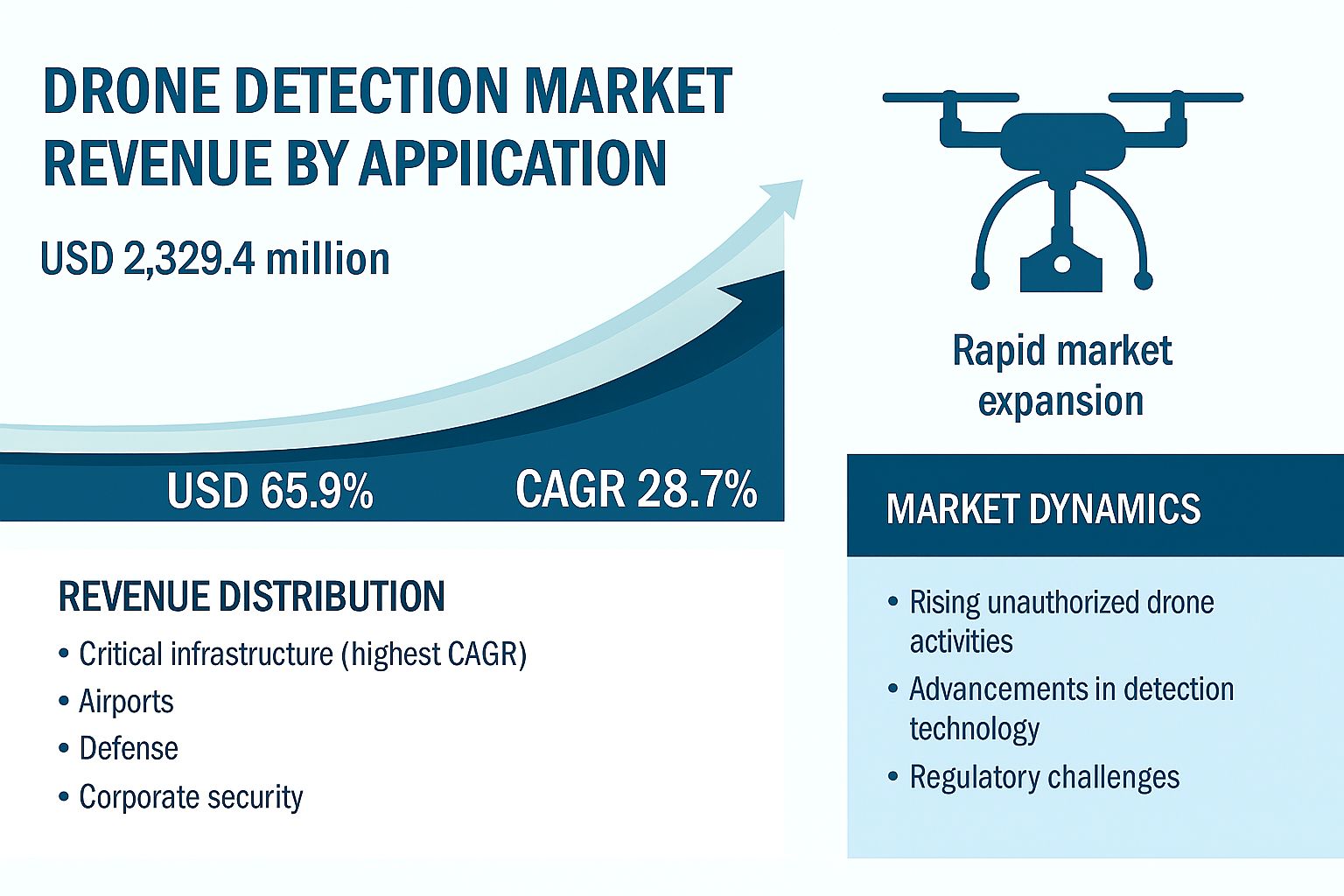

In 2024, the Drone Detection Market size is estimated at USD 659.4 million, with projections indicating it will reach USD 2,329.9 million by 2029. This translates into an impressive compound annual growth rate (CAGR) of 28.7%. Such remarkable growth is directly tied to the rising demand for real-time monitoring, counter-drone systems, and airspace protection solutions. At the heart of this expansion lies application-specific adoption, as industries including critical infrastructure, airports, military defense, and corporate security embrace drone detection systems to address evolving threats.

This blog explores Drone Detection Market revenue by application, offering a detailed breakdown of how different sectors are adopting these technologies. It further analyzes the drivers, restraints, opportunities, and challenges shaping the industry, while profiling leading players driving innovation and growth.

Market Dynamics

The Drone Detection Industry is influenced by a variety of factors. On the one hand, rising unauthorized drone activities serve as the strongest driver of demand. These drones are often used for illegal surveillance, smuggling contraband, or gathering intelligence in sensitive areas such as borders and military bases. Traditional security systems, designed to detect large aircraft or ground threats, struggle with small, low-flying drones, making specialized detection technologies essential.

On the other hand, regulatory frameworks remain a major restraint. While some countries like the US and EU nations have advanced rules supporting drone detection and counter-drone systems, others impose restrictions on radio frequency (RF) interception and jamming, limiting deployment. This creates a fragmented regulatory environment that slows adoption across borders.

Opportunities arise from technological advancements in artificial intelligence, Internet of Things (IoT), and multi-sensor fusion. These technologies enhance detection accuracy, reduce false alarms, and enable automated threat classification. Emerging swarm detection capabilities are particularly significant, as they allow security agencies to detect and respond to multiple drones operating simultaneously.

The biggest challenge, lies in cybersecurity. As detection systems increasingly rely on connected platforms and real-time data sharing, they become vulnerable to hacking, spoofing, and jamming attacks. Ensuring cybersecurity resilience will be critical for sustainable market growth.

Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=199519485

Revenue by Application

Critical Infrastructure

The critical infrastructure segment represents the fastest-growing application of the Drone Detection Market, projected to achieve the highest CAGR during the forecast period. This growth is driven by rising threats near power plants, oil and gas fields, industrial facilities, prisons, corporate headquarters, and data centers. Drones have been used for spying, sabotage, and disruptions at such facilities, endangering both economic stability and public safety.

Governments and businesses are investing heavily in advanced multi-layered detection systems combining radar, RF scanning, electro-optical sensors, and AI-driven monitoring. These solutions ensure comprehensive surveillance of restricted areas, real-time alerts, and automated responses. The introduction of regulations mandating stronger airspace protection around sensitive infrastructure has further accelerated adoption. As drone-related security incidents continue to rise, critical infrastructure will remain a primary driver of revenue growth.

Airports and Airspace Security

Airports are among the most vulnerable sites for unauthorized drone activities. Even a single drone intrusion can ground flights, disrupt operations, and compromise passenger safety. The Drone Detection Market for airport applications is expanding rapidly, as aviation authorities prioritize safeguarding airspace from intrusions.

Radar-based systems, radio frequency analyzers, and infrared imaging technologies are being deployed to monitor airport perimeters and flight paths. AI integration allows these systems to distinguish drones from birds and other airborne objects, reducing false positives. With aviation regulations becoming stricter, airport authorities worldwide are investing in scalable detection solutions to prevent incidents that could cost millions in delays and penalties.

Defense and Military Applications

Defense remains the backbone of the Drone Detection Market, accounting for the largest share of revenue. Military bases, border areas, and conflict zones face continuous threats from hostile drone activities, including surveillance, smuggling, and armed drone attacks. Governments are allocating significant budgets to enhance counter-drone capabilities with radar tracking, RF interception, electronic warfare, and kinetic systems.

Recent geopolitical tensions and regional conflicts have further accelerated military investment. Swarm detection technology is becoming especially critical for defense forces, as adversaries increasingly deploy multiple drones simultaneously. Defense-focused revenue is expected to remain strong throughout the forecast period, supported by continuous innovation and government funding.

Corporate and Event Security

Corporate entities and large public events represent an emerging application segment for the Drone Detection Market. Unauthorized drones at VIP gatherings, concerts, or sports events pose both privacy and safety risks. Similarly, corporations housing sensitive intellectual property invest in detection systems to secure their campuses.

AI-powered monitoring platforms, portable detection systems, and multi-sensor fusion are increasingly used to ensure perimeter security. As awareness of drone threats rises in the private sector, this segment will continue to contribute significantly to market revenue.

Regional Outlook

North America

North America dominates the Drone Detection Market, with revenue projected to reach USD 1,176.2 million by 2029 at a CAGR of 26.3%. The US leads due to strict airspace regulations, rising defense investments, and the adoption of AI-powered detection technologies. Canada also contributes with growing adoption in critical infrastructure and homeland security.

Europe

Europe represents a strong growth region, driven by regulatory frameworks such as EU directives requiring enhanced airspace security. Airports, military bases, and industrial facilities in countries like Germany, France, and the UK are deploying advanced detection technologies. The presence of leading companies such as Thales, Saab, and Rheinmetall further strengthens the region’s market position.

Asia Pacific

The Asia Pacific region is expanding quickly due to rising drone adoption in both commercial and defense sectors. Countries such as China, India, and Japan are investing in AI-driven and radar-based detection systems. Government initiatives to secure urban airspaces and critical assets are expected to fuel continued revenue growth.

Middle East

The Middle East, home to leading global airlines and critical energy infrastructure, is emerging as a significant market for drone detection. Nations like the UAE and Saudi Arabia are deploying systems to protect airports and oil facilities, ensuring steady growth in the coming years.

Latin America

Latin America, led by Brazil and Mexico, is adopting drone detection technologies to secure borders, critical sites, and public events. While still a smaller market compared to North America and Europe, investments are increasing steadily.

Technology Outlook

Radar systems dominate the Drone Detection Market by technology segment, accounting for the largest revenue share. Radar offers long-range surveillance and operates effectively under poor weather conditions. AI-powered radar integration further enhances real-time classification and tracking.

Radio frequency scanners and electro-optical/infrared sensors complement radar, enabling multi-sensor fusion for greater accuracy. Emerging technologies such as cognitive radar, phased array radar, and swarm detection systems are setting the stage for future market expansion.

Key Market Drivers

The rise in unauthorized drone activities is the strongest driver of the Drone Detection Market, creating urgent demand for advanced detection systems across industries. Drones used for smuggling, spying, and sabotage highlight the inadequacy of traditional security solutions and accelerate investment in AI-powered and automated platforms.

Key Restraints

Evolving regulatory frameworks represent the main restraint, as varying rules across regions limit deployment and create compliance challenges. Restrictions on RF jamming and privacy concerns with AI-based surveillance slow market adoption.

Opportunities

Technological advancements in radar, RF scanners, AI, and IoT create vast opportunities for innovation. Demand for scalable and customized solutions across critical infrastructure, airports, and defense ensures a strong outlook for technology providers.

Challenges

Cybersecurity risks remain the biggest challenge. As detection systems become more connected, they are increasingly exposed to hacking, spoofing, and data manipulation. Building cyber-resilient platforms is essential for future growth.

Key Players in the Drone Detection Market

Lockheed Martin Corporation (US): Lockheed Martin remains a global leader in defense technologies, including drone detection. The company integrates radar, electronic warfare, and AI solutions to deliver advanced airspace security systems for military and homeland defense.

RTX (US): RTX, formerly Raytheon Technologies, focuses on multi-sensor fusion and radar solutions. Its expertise in long-range surveillance ensures strong adoption across defense and airport applications.

Northrop Grumman (US): Northrop Grumman develops radar and RF interception systems that strengthen counter-drone capabilities. Its solutions are widely deployed in military and border defense operations.

Teledyne FLIR LLC (US): Teledyne FLIR specializes in electro-optical and infrared imaging technologies, playing a critical role in multi-sensor drone detection platforms. Its solutions improve accuracy in complex environments.

Elbit Systems Ltd. (Israel): Elbit Systems provides advanced counter-UAS solutions, including multi-layered detection and electronic warfare systems. Recent contracts with NATO countries highlight its strong global presence.

Thales (France): Thales combines radar, AI, and unmanned traffic management solutions to deliver advanced drone detection capabilities. Its collaborations in India and Europe expand its footprint.

Saab AB (Sweden): Saab’s Giraffe radar systems are widely used for long-range surveillance and drone detection. Recent contracts underscore its strong position in defense applications.

Leonardo S.p.A. (Italy): Leonardo develops radar and RF-based detection solutions tailored for defense and airport applications, supporting Europe’s airspace security needs.

Rheinmetall AG (Germany): Rheinmetall offers radar-based air defense and counter-drone systems, supporting military and homeland security initiatives across Europe.

L3Harris Technologies, Inc. (US): L3Harris focuses on integrating radar, EO/IR, and software platforms to deliver portable and scalable drone detection solutions.

Israel Aerospace Industries (Israel): IAI offers radar and RF-based counter-drone technologies, focusing on military defense and border security applications.

DroneShield Ltd (Australia): DroneShield develops vehicle-based and portable counter-drone systems, serving both defense and commercial sectors globally.

QinetiQ (UK): QinetiQ provides innovative RF and radar solutions for drone detection, with applications in defense, airports, and critical infrastructure.

Bharat Electronics Limited (India): BEL develops indigenous radar and RF-based detection systems, supporting India’s homeland defense and critical infrastructure protection.

ASELSAN A.S. (Turkey): ASELSAN delivers multi-sensor detection systems tailored for military defense, expanding its footprint in regional security markets.

Future Outlook

The Drone Detection Market is on track for exponential growth, driven by rising drone threats, government investments, and technological advancements. With applications spanning critical infrastructure, airports, defense, and corporate security, revenue growth will continue to diversify. By 2029, the market is expected to exceed USD 2.3 billion, with North America and Europe maintaining dominance while Asia Pacific emerges as a strong growth hub.