Counter-Drone Defense Revolution

Counter-Drone Defense Revolution: The Rise of Directed-Energy Weapon Systems

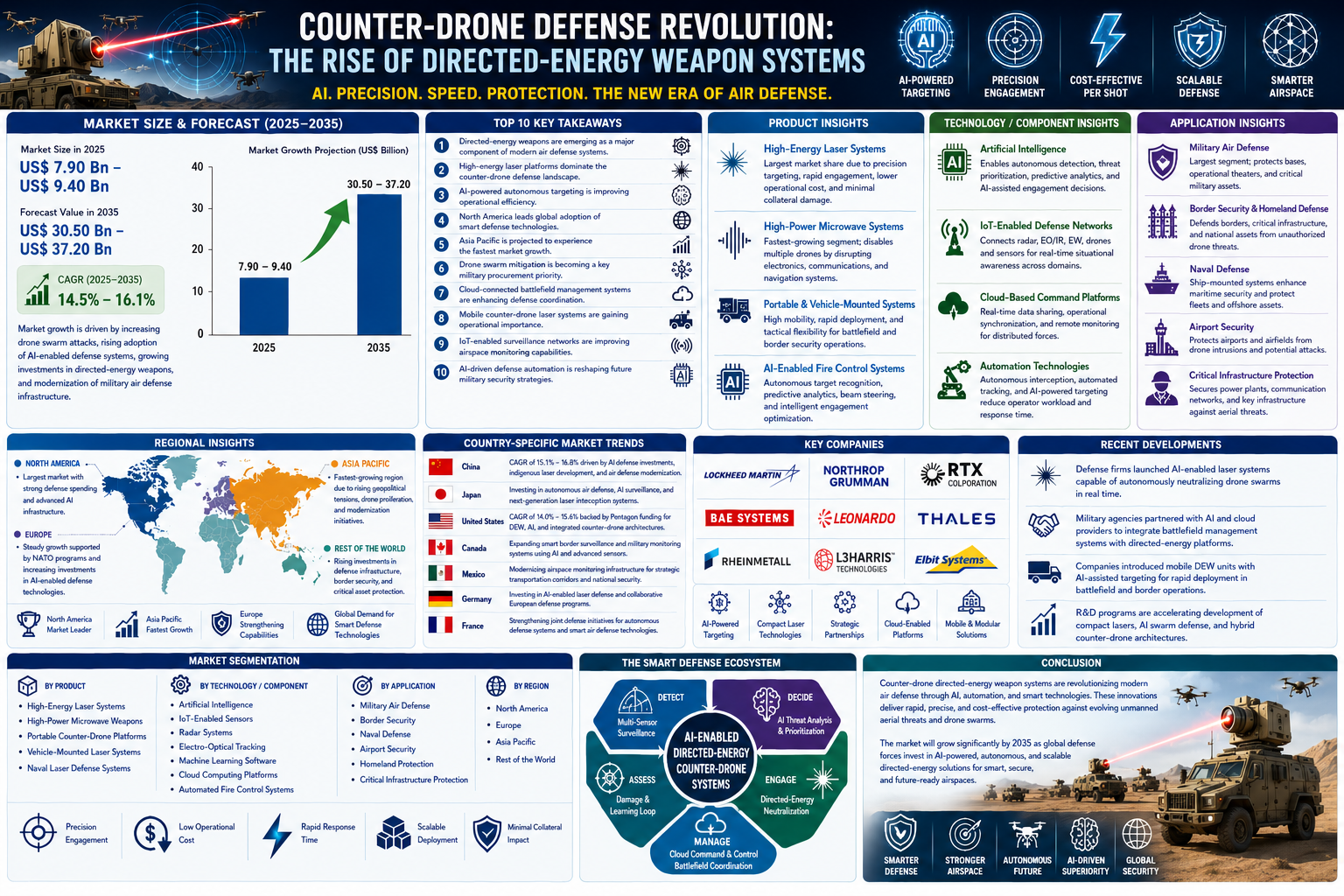

The global market for counter-drone directed-energy weapon systems is estimated to grow from US$ 7.90 Billion – US$ 9.40 Billion in 2025 to US$ 30.50 Billion – US$ 37.20 Billion by 2035 at a CAGR of 14.5% – 16.1% from 2025 to 2035. The rapid rise in drone-based threats, growing military modernization programs, and increasing deployment of autonomous aerial systems are significantly accelerating investments in next-generation counter-drone defense technologies worldwide. Directed-energy weapon systems, including high-energy lasers and high-power microwave platforms, are increasingly being adopted to neutralize unmanned aerial threats with greater speed, precision, and cost efficiency compared to conventional kinetic systems. Artificial intelligence, IoT-enabled surveillance infrastructure, automated targeting systems, and cloud-connected battlefield management platforms are transforming the operational capabilities of modern air defense ecosystems. Governments and defense agencies are investing heavily in AI-driven autonomous interception technologies, mobile laser defense systems, and integrated smart defense networks to strengthen military airspace protection and homeland security operations.

Key Market Trends & Insights

North America dominates the market due to extensive defense modernization initiatives and advanced investments in AI-enabled directed-energy weapon programs.

Asia Pacific is projected to witness the fastest market growth driven by increasing geopolitical tensions, drone proliferation, and rising indigenous defense manufacturing capabilities.

High-energy laser systems account for the largest market share because of their precision targeting capabilities and lower operational costs per engagement.

AI-powered autonomous targeting and sensor fusion technologies are transforming counter-drone air defense strategies.

IoT-enabled radar systems and cloud-based command platforms are strengthening real-time battlefield situational awareness.

Mobile and vehicle-mounted directed-energy defense systems are gaining significant demand across military and border security operations.

Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=4197284

Market Size & Forecast

- Base year market size (2025): US$ 7.90 Billion – US$ 9.40 Billion

- Forecast value by 2035: US$ 30.50 Billion – US$ 37.20 Billion

- CAGR (2025–2035): 14.5% – 16.1%

- Market growth is driven by increasing drone swarm attacks, rising adoption of AI-enabled defense systems, growing investments in directed-energy weapons, and modernization of military air defense infrastructure

Counter-Drone Defense Revolution: The Rise of Directed-Energy Weapon Systems Top 10 key takeaway

- Directed-energy weapons are emerging as a major component of modern air defense systems

- High-energy laser platforms dominate the counter-drone defense landscape

- AI-powered autonomous targeting is improving operational efficiency

- North America leads global adoption of smart defense technologies

- Asia Pacific is projected to experience the fastest market growth

- Drone swarm mitigation is becoming a key military procurement priority

- Cloud-connected battlefield management systems are enhancing defense coordination

- Mobile counter-drone laser systems are gaining operational importance

- IoT-enabled surveillance networks are improving airspace monitoring capabilities

- AI-driven defense automation is reshaping future military security strategies

Product Insights

High-energy laser systems currently represent the leading product segment in the counter-drone defense market due to their ability to neutralize unmanned aerial threats with high precision and minimal collateral damage. These systems provide military forces with scalable and cost-effective defense capabilities, especially against small drones and coordinated swarm attacks. Defense organizations are increasingly deploying laser-based platforms across military installations, naval fleets, border surveillance zones, and critical infrastructure protection networks.

High-power microwave systems are emerging as one of the fastest-growing product categories because they can disable multiple drones simultaneously by disrupting electronic components, communications, and onboard navigation systems. These systems are especially effective against complex drone swarm attacks and electronic warfare scenarios.

Portable and vehicle-mounted directed-energy systems are also gaining strong traction as armed forces seek highly mobile and rapidly deployable air defense capabilities. Lightweight laser weapon platforms integrated with armored vehicles and tactical defense units are improving battlefield flexibility and operational readiness.

Artificial intelligence is increasingly integrated into directed-energy systems through autonomous target recognition software, predictive threat analytics, automated beam steering systems, and intelligent fire control algorithms. These technologies significantly enhance response speed and targeting accuracy during high-intensity combat operations.

Technology / Component Insights (Rename based on keyword if needed)

Artificial intelligence is transforming the counter-drone defense industry by enabling autonomous threat detection, intelligent target prioritization, and AI-assisted engagement decision-making. Machine learning algorithms analyze real-time data collected from radar systems, electro-optical sensors, infrared tracking platforms, and battlefield surveillance networks to identify and neutralize aerial threats more efficiently.

IoT-enabled defense ecosystems are strengthening military airspace monitoring by integrating connected sensors, surveillance drones, radar systems, electronic warfare platforms, and command centers into unified operational networks. These interconnected systems improve situational awareness and enable faster response coordination across multiple operational domains.

Cloud-based battlefield management platforms are becoming increasingly important for managing large-scale defense operations. These systems facilitate real-time intelligence sharing, operational synchronization, and remote monitoring capabilities for distributed military forces and autonomous defense platforms.

Automation technologies are reducing operator workload while improving response efficiency in counter-drone operations. Autonomous interception systems and AI-powered tracking software enable rapid-response engagement against high-speed or swarm-based aerial threats.

Future innovation trends are expected to include compact solid-state laser systems, quantum-enhanced targeting technologies, hybrid electronic warfare integration, AI-powered swarm interception platforms, and next-generation mobile defense architectures designed for autonomous battlefield operations.

Application Insights

Military air defense applications account for the largest market share because governments worldwide are prioritizing investments in advanced counter-drone systems to protect military bases, operational theaters, strategic assets, and forward-deployed forces. Rising drone incursions and the growing use of autonomous aerial platforms in modern warfare are accelerating deployment of directed-energy defense systems.

Border security and homeland defense applications are also witnessing strong growth due to increasing threats associated with unauthorized drone surveillance, smuggling activities, and critical infrastructure attacks. Directed-energy systems provide efficient, scalable, and low-collateral defense capabilities for civilian and military airspace protection.

Naval defense applications are rapidly expanding as maritime forces integrate ship-mounted laser weapons and AI-enabled drone interception technologies into naval fleets and offshore security operations. These systems improve maritime domain awareness and strengthen protection against low-cost unmanned aerial threats.

Future opportunities are expected in airport security, urban infrastructure protection, smart military bases, autonomous battlefield defense networks, and integrated multi-domain air defense ecosystems powered by artificial intelligence and automation technologies.

Regional Insights

North America dominates the counter-drone directed-energy weapons market due to substantial defense spending, advanced military AI infrastructure, and extensive research programs focused on laser-based air defense technologies. The United States continues to lead deployment of AI-powered counter-drone systems and next-generation directed-energy defense platforms across military and homeland security operations.

Europe is experiencing steady growth supported by NATO defense modernization initiatives, increasing investments in autonomous military technologies, and rising concerns over drone-based threats targeting critical infrastructure and defense assets. Germany, France, and the United Kingdom are expanding indigenous development programs for smart defense systems and laser weapon technologies.

Asia Pacific is projected to register the fastest growth during the forecast period due to increasing geopolitical tensions, expanding military modernization programs, and rising adoption of indigenous counter-drone technologies across China, Japan, India, and South Korea. Governments across the region are prioritizing AI-driven air defense systems and smart battlefield automation technologies.

The Middle East is also emerging as an important regional market due to rising investments in critical infrastructure protection, smart city security, and advanced military defense technologies.

- North America remains the global leader in directed-energy defense deployment

- Asia Pacific is projected to achieve the fastest market expansion through 2035

- Europe is strengthening investments in AI-powered military defense systems

- Naval laser weapon deployment is increasing across global maritime forces

- Autonomous air defense systems are becoming central to modern military operations

[Country]-Specific Market Trends

China is projected to grow at a CAGR of 15.1% – 16.8% due to extensive investments in AI-enabled defense systems, indigenous laser weapon development, and military modernization initiatives focused on autonomous warfare capabilities. The country is expanding domestic manufacturing of counter-drone technologies to reduce dependence on foreign defense suppliers.

Japan is accelerating investments in autonomous air defense systems and AI-powered surveillance technologies to strengthen maritime security and homeland defense operations. Government-supported innovation programs are advancing deployment of next-generation laser interception platforms.

The United States remains the largest national market with a CAGR of 14.0% – 15.6%, supported by significant Pentagon investments in directed-energy weapons, AI-assisted battlefield management systems, and integrated counter-drone architectures. Canada is increasing deployment of smart border surveillance technologies, while Mexico is modernizing airspace monitoring infrastructure around strategic transportation corridors.

Germany and France are strengthening collaborative defense initiatives focused on autonomous defense technologies, electronic warfare integration, and AI-enabled laser defense systems to improve European defense resilience.

- China is rapidly expanding indigenous smart defense manufacturing capabilities

- Japan is prioritizing autonomous maritime and air defense modernization

- The United States dominates global investment in directed-energy defense technologies

- Germany and France are accelerating European military AI collaboration programs

- Government-supported AI defense initiatives continue driving market expansion worldwide

Key Company Insights

Major companies operating in the market include Lockheed Martin, Northrop Grumman, RTX Corporation, BAE Systems, Leonardo, Thales Group, Rheinmetall, L3Harris Technologies, and Elbit Systems.

These companies are investing aggressively in AI-assisted targeting systems, compact laser weapon technologies, mobile counter-drone defense platforms, and autonomous interception software. Strategic partnerships with military agencies and defense ministries are accelerating commercialization of advanced directed-energy systems.

Industry participants are also focusing on modular system architectures, cloud-based battlefield integration platforms, and advanced sensor fusion technologies to improve operational efficiency across multi-domain defense environments.

- AI-powered autonomous targeting remains a major innovation priority

- Defense companies are investing heavily in compact solid-state laser systems

- Strategic defense partnerships are accelerating technology deployment worldwide

- Cloud-connected defense platforms are improving operational coordination

- Modular mobile defense architectures are gaining strong military demand

Recent Developments

Defense technology firms recently introduced AI-enabled laser defense systems capable of autonomously identifying and neutralizing drone swarm attacks in real time.

Several military organizations announced partnerships with AI software providers to integrate cloud-based battlefield management systems into next-generation counter-drone defense networks.

Leading defense contractors launched mobile directed-energy systems equipped with intelligent tracking algorithms and automated target prioritization capabilities for rapid battlefield deployment.

Market Segmentation

The market is segmented by product, technology/component, application, and region. By product, the market includes high-energy laser systems, high-power microwave weapons, portable counter-drone platforms, vehicle-mounted laser systems, and naval laser defense systems. High-energy laser systems currently dominate due to operational precision and cost-effective engagement capabilities.

By technology/component, the market includes artificial intelligence, IoT-enabled sensors, radar systems, electro-optical tracking technologies, machine learning software, cloud computing platforms, and automated fire control systems. AI-assisted targeting and automation technologies represent the fastest-growing technology category.

Applications include military air defense, homeland security, naval defense, border surveillance, airport security, and critical infrastructure protection. Military airspace defense remains the largest application segment because of rising deployment of autonomous counter-drone systems across modern warfare operations.

Regionally, the market is segmented into North America, Europe, Asia Pacific, and the rest of the world. North America currently leads the market, while Asia Pacific is projected to witness the strongest long-term growth.

- High-energy laser systems dominate the product landscape

- AI-powered targeting technologies are driving smart defense modernization

- Military air defense remains the largest application segment

- IoT-connected surveillance systems are improving situational awareness

- Asia Pacific is expected to emerge as the fastest-growing regional market

Conclusion

The counter-drone defense revolution is reshaping modern military airspace security through rapid adoption of directed-energy weapon systems, artificial intelligence, and autonomous defense technologies. Rising drone threats, expanding military modernization initiatives, and growing investments in AI-enabled air defense systems are accelerating demand for next-generation smart defense platforms worldwide.

Artificial intelligence, IoT-enabled surveillance networks, cloud-based battlefield management systems, and automation technologies are significantly improving operational efficiency, response speed, and autonomous threat engagement capabilities across modern defense ecosystems.

The market is expected to experience substantial growth through 2035 as governments and defense agencies continue investing in scalable, intelligent, and highly precise counter-drone defense technologies. Companies capable of delivering integrated AI-powered directed-energy systems and autonomous battlefield defense architectures are expected to maintain strong competitive positioning in the evolving global smart defense industry.