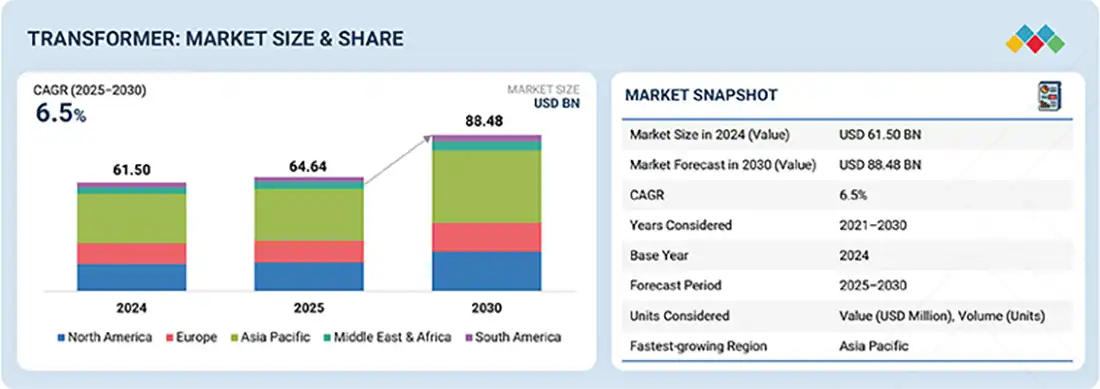

The global transformer industry is estimated to be valued at USD 64.64 billion in 2025 and is projected to reach USD 88.48 billion by 2030, growing at a CAGR of 6.5%. This growth is driven by the rising global demand for reliable and efficient electricity infrastructure, increasing investments in grid modernization, and the rapid integration of renewable energy sources. Additionally, industrial expansion, urbanization, and the electrification of transportation and manufacturing sectors significantly boost the need for high-performance transformers. Technological advancements, such as smart transformers and eco-friendly insulation systems, also contribute to market growth, as end users seek energy-efficient and sustainable power solutions.

Download PDF Brochure – https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=261783147

One of the most impactful advancements reshaping the transformer market landscape is the growing adoption of digital and smart transformers equipped with real-time monitoring, predictive maintenance, and automated control features. These intelligent systems use IoT sensors, cloud analytics, and AI-based diagnostics to enhance grid reliability, reduce downtime, and optimize energy efficiency, making them especially valuable in critical infrastructure such as data centers and urban substations. Additionally, regulatory shifts in environmental standards, particularly in Europe and North America, push manufacturers to adopt eco-efficient designs, such as transformers with bio-based insulating fluids and SF₆-free gas insulation systems to reduce greenhouse gas emissions. These developments necessitate substantial technological innovation while paving the way for new business models focused on digital services, performance-based contracting, and sustainability-oriented procurement. These shifts transform the competitive landscape and redefine how companies create and deliver value in a rapidly evolving market.

With a significant portion of the country’s transmission and distribution network aging beyond its intended lifespan, the US is channeling substantial federal and state-level funding, such as through the Infrastructure Investment and Jobs Act, into upgrading substations, replacing legacy transformers, and enhancing grid resilience. The rapid deployment of renewable energy projects, particularly in solar- and wind-rich states such as Texas and California, further intensifies the demand for high-efficiency and digitally enabled transformers. Additionally, the growing proliferation of electric vehicles, data centers, and smart grid technologies is transforming the nature of energy consumption, prompting utilities and private players to invest in advanced transformer solutions that can support dynamic loads and real-time monitoring. This combination of infrastructure needs, policy momentum, and technological advancement firmly positions the US as the growth engine of the transformer market.

In North America, by type, distribution transformers are projected to record the highest CAGR during the forecasted period, driven by the region’s intensified focus on strengthening last-mile power delivery and supporting the decentralization of energy systems. As utilities across the US and Canada work to replace aging grid infrastructure and extend services to growing suburban and rural communities, the need for modern, efficient, and low-maintenance distribution transformers has surged. Also, the widespread deployment of distributed energy resources (DERs) such as rooftop solar, battery storage, and electric vehicle (EV) charging infrastructure is placing new performance demands on distribution networks. This shift requires transformers to be more responsive to bidirectional power flows and capable of real-time load balancing. In response, utilities increasingly turn to smart distribution transformers with monitoring, fault detection, and grid optimization capabilities. Additionally, the growing number of data centers, commercial facilities, and residential electrification initiatives, particularly in Texas, California, and New York, is boosting demand for compact and efficient distribution units. These drivers, combined with supportive policies such as the Grid Resilience and Innovation Partnerships (GRIP) program, position the distribution transformer segment as a cornerstone of grid modernization in North America.

Make an Inquiry – https://www.marketsandmarkets.com/Enquiry_Before_BuyingNew.asp?id=261783147

Players in the transformer market are actively tapping into emerging opportunities by aligning their strategies with key industry trends such as digitalization, sustainability, grid modernization, and the rapid expansion of renewable energy. As countries commit to decarbonization and invest in smart, resilient energy systems, demand is surging for advanced transformers that support digital monitoring, bidirectional power flows, and eco-friendly materials. Major players, including Hitachi Energy Ltd. (Switzerland), Siemens Energy (Germany), Eaton (Ireland), GE Vernova (US), and Toshiba Energy Systems & Solutions Corporation (Japan), can capitalize on these opportunities by expanding their portfolios of smart and solid-insulated transformers, investing in R&D for digital and AI-integrated systems, and forming strategic partnerships with utilities and governments to participate in large-scale modernization projects. Furthermore, companies that localize manufacturing, offer end-to-end services (such as predictive maintenance and remote diagnostics), and align with tightening regulatory standards, particularly around energy efficiency and environmental impact, are well-positioned to secure long-term contracts and strengthen their global market presence. By proactively adapting to the evolving energy ecosystem, large players can move beyond traditional supply roles and become key enablers of the worldwide energy transition.