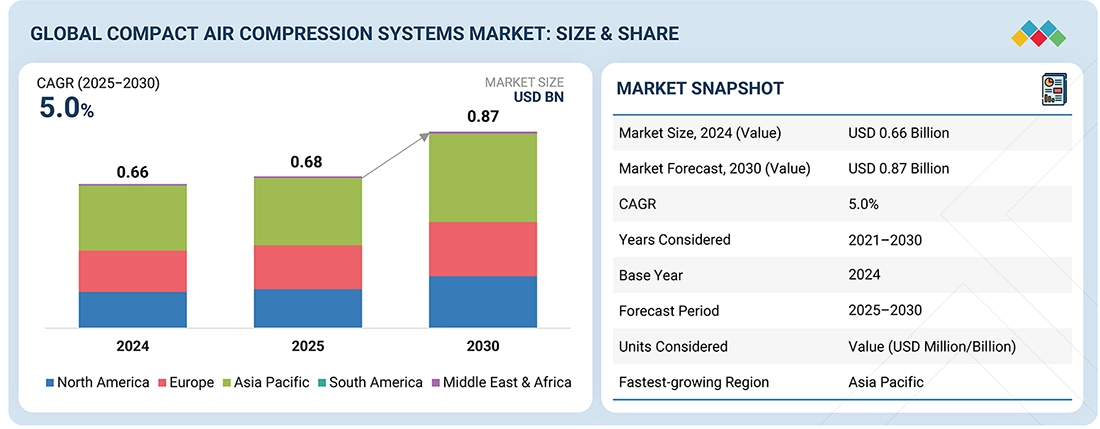

The report “Compact Air Compression Systems Market By Product Type (Positive Displacement Blowers, Side Channel Blowers, Dry Vane Pumps, Claw Pumps), Pressure (0.1–0.4 bar(g), 0.4–0.8 bar(g)), End User (Wastewater Treatment), and Region – Global Forecast to 2030” The compact air compression system market is projected to reach USD 0.87 billion by 2030 from USD 0.68 billion in 2025, at a CAGR of 5.0% over the forecast period.

There are a few important factors that drive the market. Governments all over the world are putting strict rules in place for energy efficiency and industrial sustainability to lower energy use and emissions. The minimum energy performance standards (MEPS) and eco-design directives are two of these policies. They push different industries to use compressors and blowers that use less energy. More and more businesses are trying to use energy more efficiently and cut costs, especially in areas like low-pressure air systems and wastewater aeration. To meet rules and become more efficient, businesses are using small, energy-efficient, and oil-free air compression systems. New technologies like variable speed drives and digital monitoring systems are making things work better and more reliably. These advancements help companies comply with changing industry standards, which boosts the demand for compact air compression systems.

Industries are increasingly placing a greater emphasis on energy efficiency and sustainability in their operational and investment decisions. This trend is resulting in businesses adopting compact compressed air systems (such as reciprocating or rotary screw compressors) that minimize energy consumption and improve efficiency within an overall process. A growing focus on energy optimization is also driving demand for new compressed air technologies as well as for industrial manufacturing. There are many new developments in technology that have been implemented in the design of compressed air systems that enhance the performance, reliability, and efficiency of these systems. Examples of some of these technologies include variable speed drives (VSDs) to optimize airflow; oil-free (or dry-type) compressors to eliminate the need for lubricating oils; and digitally enabled monitoring solutions to allow for real-time monitoring and predictive maintenance of compressed air systems. In addition, an increasing amount of governmental regulation focusing on energy efficiency and emissions reduction is also motivating manufacturers across all industries to adopt more energy-efficient compressed air systems. By establishing efficiency standards and environmental regulations, governmental agencies and regulatory bodies are supporting sustainable industrial practices. As industrial companies continue to make strong commitments to both sustainability and operational efficiency, there will be an increasing demand for advanced, reliable, and energy-efficient compact compressed air systems in the global marketplace.

Download PDF Brochure @ https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=108364830

The 0.1–0.4 bar (g) segment, by pressure, is estimated to account for the second-largest share of the compact air compression system market.

The 0.1–0.4 bar (g) segment, by pressure, is projected to have the second-largest market share in the compact air compression equipment market due to the pressure segment being most frequently utilized in the wastewater treatment (WWT), aquaculture, pneumatic conveying, and other low-pressure industrial applications. The 0.1–0.4 bar (g) has become one of the leading segments within the global compact air compression equipment market because of how it can generate continuous airflow while minimizing energy use and costs to operate, and is readily available to provide continuous airflow even if running continuously under normal operating conditions. Several factors driving demand for this segment include increasing adoption of energy-efficient systems, increased use of blowers that provide low-pressure airflow, and manufacturers wanting to optimize energy consumption and reduce costs of operation; all these manufacturers will benefit by providing compact, low noise, and oil-free solutions for air compression with enhanced performance and reliability within a 0.1–0.4 bar (g) pressure environment creating an even stronger demand for the 0.1–0.4 bar (g) pressure segment.

Europe is projected to emerge as the second-largest compact air compression system market.

The primary driver of the compact air compression systems market in Europe is that Europe has implemented very stringent energy-efficiency compliance requirements; there are numerous regulations regarding eco-design and energy-efficiency standards for compressors. Most notably, many companies in all industries have adopted advanced manufacturing processes and have made significant investments in manufacturing technology. Europe also has a very well-established industrial base, such as the food and beverage, pharmaceutical, automotive, and wastewater treatment sectors. A well-established industrial base creates consistent demand for compact, reliable air compression systems, which further enhances market demand. Companies across Europe are placing greater emphasis on reducing the costs associated with operations and energy consumption, thereby accelerating the adoption of oil-, low-pressure, and low-efficiency compressed air systems. Additionally, companies are benefiting from the continued development of new technologies, along with the presence of many of the world’s top manufacturers of compact air compressors located in Europe.

Ask Sample Pages of the Report @ https://www.marketsandmarkets.com/requestsampleNew.asp?id=108364830

Key Players

Key players in the global compact air compression system market include Atlas Copco AB (Sweden), Ingersoll Rand Inc. (US), KAESER KOMPRESSOREN (Germany), KUBÍCEK VHS, s.r.o. (Czech Republic), Busch Vacuum Solutions (Germany), Becker Pumps (Germany), Goorui (China), Usha Neuros Turbo LLP (India), Fans and Blowers (UK), Elektror (Germany), Rexblower (China), Rico Druckluftanlagenbau GmbH (Germany), Induvac (Netherlands), and SEKO S.p.A. (Italy).